Over the past few years the media has provided a lot of coverage on cryptocurrencies and blockchain, focusing primarily on the astronomical rise and fall in value of Bitcoin, leaving most of us confused about what blockchain technology is and what its value is. This article will provide an insight into this disruptive technology.

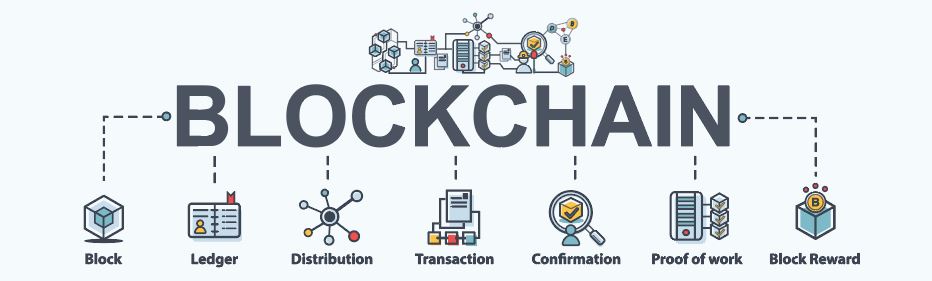

Blockchain is best defined as a digital ledger that cannot be altered once a transaction has been input and verified.

Each party involved in this transaction maintains a copy of this ledger, storing information, such as a timestamp, and the transactional data. This is protected by cryptography, meaning no transaction can be amended.

The adoption of blockchain technology has been primarily recognized for the thousands of cryptocurrencies that have been created, rather than the transparent and secure manner of processing transactions through the blockchain network. Blockchain also has no transaction cost meaning that, once adopted into a business model, it can replace the need to charge a transaction fee.

In 2018 there was a rise in companies across different sectors investing in blockchain technology, with an anticipated growth within the market to $60 billion by 2024. Firms such as Goldman Sachs, J.P. Morgan and Lloyds have spent over $30milion in blockchain start-ups. Aside from investments in banking and finance there are countless blockchain projects across multiple sectors; including law, healthcare and agriculture.

Several of the world’s leading food suppliers, including Nestle, Unilever, Dole and Walmart, are partnering with IBM to create a global food tracing system on blockchain, allowing visibility of the origins of potentially hazardous goods and any sources of contamination. This is intended to further strengthen consumer confidence in the global food system.

As more successful projects emerge, many industries are proactively seeking new ways to incorporate blockchain technology.

Prior notions of blockchain being a threat to banks have been minimized due to several user cases evidencing that the decentralized system of the blockchain network ensures that information of value does not have a centralized point of access. Therefore making it less susceptible to data leakage or alteration. As a result, it is less likely for online payments or a bank’s website to be hacked and for there to be a breach of personal information.

The digital currencies used in blockchain enables transactions to be completed in just a few minutes, whereas this typically takes a minimum of two days for differing banks. This improved efficiency allows parties to complete transactions without an intermediary, therefore reducing the dependents on time consuming and expensive financial institutions.

Financial institutions’ original scepticism on blockchain initially arose as it was viewed as a direct competitor to the traditional banking process. The idea that the anonymity of this technology is attractive to criminals made the adoption of this technology slow; and this was worsened by the surge and crash of interest in cryptocurrency causing the digital currency to appear as a “hoax”.

In reality, the application of blockchain can solve countless security challenges across various sectors but it is not a complete solution. Looking at the positives, blockchain operates on a decentralized network and the data stored can be tracked – with blockchain ensuring that it is immutable and cannot be tampered with.

To reap the benefits of this technology, businesses need to integrate, develop and update blockchain technology regularly for optimal results. There will be a continual growth in the adoption of blockchain across various industries to ensure competitiveness and efficiency.

At Concilium Search we have built a team that focusses on blockchain, partnering with several organisations and adopting the technology to assist with their resourcing requirements.

If you are require any additional information or are interested in working with our Technology department, please contact carlin.debrah@conciliumsearch.com

Carlin Debrah

Post a Comment